30-Day No-Spend Challenge: A Practical Starter Guide

Discover how a 30-day no-spend challenge can reset your spending habits, strengthen financial discipline, and boost long-term savings.

In an age of subscription overload and easy one-click purchases, managing personal finances has become increasingly challenging for Americans. Whether you’re an individual trying to regain control over your budget or a professional seeking smarter financial habits, the no-spend challenge offers a practical and impactful reset.

The 30-day no-spend challenge isn’t about deprivation — it’s about mindfulness. It invites participants to pause unnecessary spending for a month, allowing them to reflect on priorities, reduce financial stress, and rediscover value beyond consumerism. As 2025 continues to present economic uncertainties — from inflation fluctuations to the rapid evolution of digital banking and B2B payments — learning to manage cash flow effectively has never been more crucial.

This guide provides a clear, step-by-step framework for anyone looking to start a no-spend challenge, supported by proven strategies, behavioral insights, and actionable tips tailored to the current financial landscape in the United States. Whether you’re tackling debt, building savings, or optimizing your household or business budget, this 30-day journey can transform how you think about money — one intentional choice at a time.

Understanding the No-Spend Challenge

At its core, the no-spend challenge is a personal finance experiment designed to help individuals and even small businesses curb impulsive expenditures. The goal is simple: avoid non-essential purchases for a set period, typically 30 days, while spending only on necessities such as housing, utilities, and groceries.

This challenge differs from extreme frugality because it focuses on awareness rather than denial. By temporarily pressing pause on discretionary spending, you develop a deeper understanding of your financial habits. It’s a powerful way to confront questions like: What do I truly need? What triggers my spending? How much can I save if I cut the excess?

In 2025, the challenge aligns perfectly with broader financial trends. As more Americans use digital banking platforms and financial automation tools, transparency around expenses is easier than ever. Through apps that categorize spending or offer cash flow insights, participants can monitor their progress in real time, making the challenge not only manageable but measurable.

Ultimately, this experiment teaches self-control, reshapes priorities, and paves the way toward long-term financial health — both personally and professionally.

Why a 30-Day Period Works Best

A 30-day time frame strikes the right balance between challenge and sustainability. It’s long enough to disrupt old patterns yet short enough to remain achievable. Behavioral economists have shown that habits can start to form in as little as three weeks, and a one-month period allows participants to witness measurable outcomes — from improved savings to heightened financial confidence.

In corporate finance and cash management, the same principle applies. Short-term restrictions on nonessential spending can lead to longer-term efficiency gains. Businesses often use quarterly or monthly reviews to optimize resources; the no-spend challenge mirrors this logic on a personal level.

Psychologically, a 30-day challenge feels less intimidating than a year-long restriction. It promotes consistency without fatigue. Moreover, it encourages participants to engage with the process as a learning opportunity rather than a punishment.

As inflation and cost-of-living pressures persist in 2025, adopting a month-long financial reset can be a practical, low-risk way to adapt to changing economic conditions while building resilience against future uncertainties.

Setting Clear Rules for Success

Before starting your no-spend challenge, it’s essential to define your boundaries clearly. The most successful participants plan every detail:

- Identify essentials: Rent, utilities, groceries, healthcare, and transportation.

- List exclusions: Dining out, streaming subscriptions, impulse online shopping, and non-urgent upgrades.

- Establish exceptions: Planned commitments like birthdays or medical appointments.

- Use tools: Budgeting apps or spreadsheets for tracking daily progress.

Clarity prevents loopholes and maintains accountability. It also makes the challenge customizable — for example, corporate teams can adapt it to manage business expenses, focusing on non-critical costs like travel or entertainment.

By setting structured rules, you transform the challenge into a disciplined financial strategy. This step builds a foundation for better cash management, much like businesses use budgetary controls to enhance profitability. When individuals treat their personal finances with the same strategic mindset, the results are often transformative.

Building a Realistic Budget Before You Start

Success in a no-spend challenge depends on preparation. Start by creating a detailed budget that distinguishes fixed, variable, and discretionary expenses. This snapshot reveals where your money flows each month and which categories offer the greatest potential for savings.

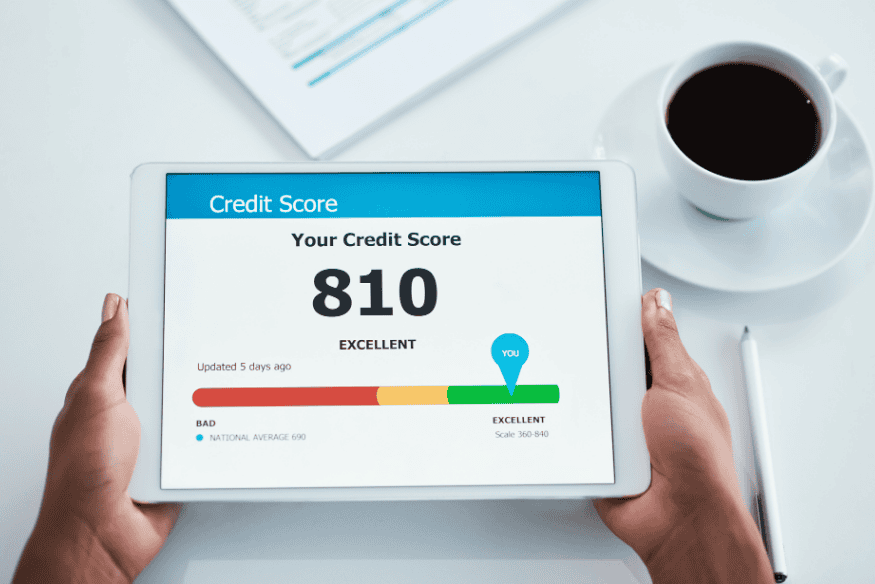

In the 2025 financial environment — characterized by fluctuating interest rates and evolving banking incentives — budgeting tools have become more sophisticated. Platforms like Mint, Monarch Money, and YNAB integrate with digital banks and offer instant visualizations of spending patterns. These insights can make your challenge smoother and more transparent.

Set specific goals for your 30 days: Are you saving for an emergency fund, reducing credit card debt, or preparing for a large purchase? Clear objectives keep motivation high and provide measurable outcomes.

By grounding your challenge in a realistic budget, you establish control over your cash flow — a concept equally vital in corporate finance and B2B payment management. Whether managing a household or a business account, a well-structured budget is the backbone of financial stability.

Smart Substitutes for Everyday Spending

Eliminating nonessential purchases doesn’t mean sacrificing comfort or joy. The no-spend challenge encourages creativity in finding free or low-cost alternatives:

- Replace dining out with home-cooked meals and meal prep.

- Opt for public parks, libraries, or local events instead of paid entertainment.

- Try clothing swaps or upcycling instead of shopping new.

- Use free online resources for learning or fitness.

Many Americans find that adopting minimalism enhances satisfaction rather than reducing it. The challenge often leads to a sense of empowerment — realizing that fulfillment doesn’t depend on constant consumption.

For professionals or small business owners, similar principles apply. For instance, instead of expensive conferences, teams can leverage webinars or digital workshops. Reducing unnecessary corporate spending can strengthen financial strategy and increase profitability.

Ultimately, smart substitution transforms financial restraint into an exercise in innovation and intentional living.

How to Track and Measure Your Progress

Accountability is the backbone of the no-spend challenge. Tracking ensures you stay aligned with your goals and recognize your achievements.

Daily or weekly check-ins can be as simple as jotting down expenditures in a notebook or using automated tracking apps. Some participants prefer visual aids, like progress charts or savings thermometers, to stay motivated.

On a larger scale, financial institutions and corporate treasurers apply similar tracking systems to monitor cash flow and optimize liquidity. Adopting a comparable approach in personal finance reinforces discipline and provides tangible feedback.

At the end of each week, assess what worked and what didn’t. Did you face temptation? Were there unexpected expenses? Reflection transforms mistakes into learning opportunities.

In 2025, digital ecosystems make monitoring easier than ever. From AI-powered financial assistants to mobile banking dashboards, Americans have unprecedented tools for real-time insight — a major advantage for those embracing mindful money habits.

Overcoming Common Challenges and Temptations

Every participant encounters obstacles during the no-spend challenge — impulse triggers, social pressures, or emotional spending. Recognizing these challenges early helps you prepare effective countermeasures.

Common triggers include online shopping ads, social outings, or stress-induced purchases. Combat them by unsubscribing from marketing emails, setting screen time limits, and choosing accountability partners.

Emotional spending is particularly relevant in today’s fast-paced society. Instead of turning to retail therapy, find healthier outlets such as exercise, journaling, or connecting with friends.

For professionals, workplace culture can also encourage unnecessary spending, from frequent coffee runs to team lunches. Setting shared financial goals or introducing company-wide “no-expense days” can foster collective discipline and financial awareness.

The key is not perfection but persistence. Each time you resist a temptation, you reinforce financial resilience — a skill that pays dividends long after the challenge ends.

The Psychological and Emotional Benefits

Beyond saving money, the no-spend challenge offers deep psychological rewards. It promotes mindfulness, self-awareness, and a renewed sense of control.

Studies in behavioral economics suggest that conscious restraint activates decision-making regions in the brain, improving long-term financial judgment. The satisfaction of resisting instant gratification can increase dopamine levels associated with accomplishment and self-discipline.

Moreover, reducing financial clutter can relieve stress. In 2025, when the average American household debt remains high, simplicity can be a powerful antidote to financial anxiety. Participants often report feeling lighter, more focused, and more confident in managing their finances after completing the challenge.

Businesses can benefit too. Encouraging departments to review expenses mindfully fosters a culture of efficiency and accountability — qualities that strengthen corporate finance performance.

In short, this 30-day exercise cultivates not just financial health, but emotional balance and cognitive clarity.

Turning the Challenge into a Long-Term Habit

The greatest value of the no-spend challenge lies in its lasting impact. When the 30 days end, the insights gained can shape sustainable financial habits.

Review your experience: What purchases did you truly miss? Which ones felt unnecessary? Use these reflections to build a more intentional spending plan. Consider extending the challenge by introducing regular “no-spend weekends” or “minimalist months.”

For businesses, similar practices exist under the concept of continuous improvement. Reviewing expense reports and identifying inefficiencies can lead to long-term cost reductions and stronger cash management.

Establish new habits such as automatic savings transfers or budget reviews at the end of each month. Reinforcing these behaviors ensures that the challenge’s benefits compound over time, improving not only your savings rate but also your overall financial strategy.

With consistency, what began as a 30-day reset can evolve into a lifelong mindset of intentional and strategic spending.

Applying the No-Spend Challenge in a Business Context

Although traditionally personal, the no-spend challenge has powerful applications in business environments — particularly in 2025’s competitive B2B economy. Corporate leaders and financial managers can adopt the same principles to identify inefficiencies in their organizations.

By pausing discretionary spending — such as travel, consulting, or non-critical subscriptions — companies can reveal hidden costs and improve liquidity. Many firms use “spending freezes” during periods of restructuring or when aligning resources with strategic priorities.

Digital banking and automation tools simplify this process by offering real-time analytics across departments, helping businesses track and optimize expenditure. This mirrors the personal challenge’s focus on awareness and accountability, scaled to corporate finance.

Integrating a no-spend framework into B2B cash management strategies fosters resilience, efficiency, and sustainable growth. In today’s volatile market, that level of financial discipline can provide a crucial competitive edge.

The Economic Relevance of the No-Spend Challenge in 2025

The no-spend challenge is not just a personal budgeting trend — it reflects larger economic realities in 2025. With inflation still hovering above pre-pandemic levels and consumer debt reaching record highs, many Americans are re-evaluating their relationship with spending.

Financial institutions report increased demand for digital budgeting tools, while the U.S. banking sector continues to promote cash management and financial literacy programs. This environment has made no-spend initiatives both timely and transformative.

In corporate finance, the same shift is visible. Companies are prioritizing liquidity, revising B2B payment structures, and automating treasury functions to withstand market volatility. The discipline learned through no-spend principles mirrors these professional strategies — making it a practical model for both individuals and organizations.

By embracing mindful spending and adopting efficient resource allocation, Americans can contribute to broader financial stability. The challenge is not just about saving money — it’s about adapting to a new economic era that values sustainability, intentionality, and strategic decision-making.

Conclusion

The 30-day no-spend challenge is more than a budgeting experiment — it’s a mindset shift toward intentional living and strategic financial control. By pausing unnecessary expenses, you gain clarity, discipline, and renewed appreciation for what truly matters.

In 2025, as Americans navigate inflation, digital transformation, and changing work patterns, mastering personal and corporate cash flow is more important than ever. This challenge offers a practical, low-risk way to strengthen financial health and cultivate sustainable habits.

Whether you’re an individual resetting your spending habits or a business leader rethinking cost structures, the no-spend challenge delivers one timeless lesson: control isn’t about restriction — it’s about empowerment.

Start today, and let 30 days reshape your financial future.