Best Credit Cards for Beginners in the United States

Discover how to choose the best credit cards for beginners in the U.S. and build strong credit safely from your first card.

Starting your credit journey in the United States can feel overwhelming. For many people, credit cards are the first real step into the financial system, yet the rules, fees, and long-term consequences are rarely explained clearly. Choosing the right product at the beginning matters more than most realize. The first card you open helps shape your financial habits, influences how lenders perceive you, and sets the foundation for everything from car loans to mortgages later on.

For newcomers to credit, the main challenge is balancing access and responsibility. Lenders want evidence that you can manage borrowed money, but novice usually lack a credit history. This creates a paradox where approval feels difficult just when guidance is needed most. Fortunately, the U.S. market offers several card types designed specifically to address this gap. Understanding how they work can help you avoid unnecessary costs and long-term mistakes.

This guide focuses on credit cards for beginners and explains how to evaluate them beyond flashy promotions. You will learn how entry-level cards differ from standard products, what features truly matter in the early stages, and how to use a first card to build trust with lenders instead of debt. The goal is not just approval, but sustainable progress toward a healthy credit profile.

By the end of this article, you will understand which card categories are best for learner, how to compare them responsibly, and how to use your first credit line as a long-term financial tool rather than a short-term convenience.

Understanding What Beginners Need From a First Credit Card

For someone new to credit, the primary purpose of a first card is not rewards or luxury benefits. It is to establish a positive and reliable credit history. This means the ideal product prioritizes simplicity, transparency, and predictability over complex structures or aggressive incentives.

Beginners benefit most from cards with straightforward terms. Clear interest rates, easy-to-understand statements, and predictable billing cycles reduce the risk of confusion. Complicated reward structures can distract from the core habit that matters most early on, which is consistent, on-time payment.

Another key consideration is cost. Many entry-level cards minimize or eliminate annual fees. While interest rates may still be high, responsible use and full monthly payments make those rates largely irrelevant. What matters is avoiding hidden fees or penalties that can derail progress.

Credit limits are typically lower for novice, which can actually be an advantage. Modest limits encourage disciplined spending and reduce the temptation to carry large balances. Over time, responsible use often leads to automatic credit limit increases, signaling growing trust from lenders.

Access to basic account tools also matters. Mobile apps, spending alerts, and easy payment options help novice stay organized and avoid missed due dates. These features support healthy habits and reinforce consistency.

Ultimately, the best starting point is a card that aligns with learning and stability. Learner should view the first card as a training ground rather than a source of purchasing power.

Secured Credit Cards as a Starting Point

Secured cards are one of the most accessible options for beginners who have no credit history or limited financial documentation. These cards require a refundable cash deposit that typically becomes the credit limit. From a lender’s perspective, the deposit reduces risk, making approval easier and lowering the barrier to entry for first-time applicants.

Despite the upfront deposit, secured cards function much like traditional credit cards. Purchases are reported to major credit bureaus, monthly statements are issued, and regular payments build credit history over time. This makes them a practical bridge into the credit system and a learning tool for responsible usage habits.

One advantage of secured cards is predictability. Because the credit limit matches the deposit, spending boundaries are clear. This structure encourages cautious use and helps novice understand how balances, utilization, and payments affect their profile over successive billing cycles.

Many secured cards now include pathways to upgrade to unsecured accounts. After several months of responsible use, issuers may return the deposit and convert the account, preserving the account age and positive history already established.

However, not all secured cards are equal. Some charge annual fees or impose restrictions that limit their value. Novice should focus on products that report to all major bureaus and offer a clear upgrade path.

Used correctly, secured cards are not a setback but a strategic step. They allow learner to demonstrate reliability in a controlled environment before moving on to more flexible products with confidence.

Student Credit Cards and Their Unique Advantages

Student cards are designed for individuals enrolled in higher education who may lack established credit but have verifiable enrollment status. These cards recognize future earning potential rather than past credit behavior, aligning approval decisions with long-term prospects instead of limited financial history.

One defining feature of student cards is accessibility. Issuers often use academic enrollment as a substitute for traditional credit requirements. This makes them particularly appealing for young adults starting their financial independence while balancing studies and limited income sources.

Student cards often include educational tools. Many provide resources on budgeting, credit usage, and financial planning. These features help cardholders understand how daily decisions impact long-term outcomes and encourage healthier habits from the start.

Rewards on student cards are usually modest but attainable. Simple cash back on everyday categories can provide small incentives without encouraging overspending. Importantly, these benefits should never replace disciplined repayment or careful monitoring of balances.

Some student cards include incentives for good academic performance or consistent on-time payments. While the monetary value may be limited, they reinforce positive behavior patterns and accountability.

As graduation approaches, student cards often transition into standard entry-level cards. Maintaining the account through this transition can preserve credit age and strengthen continuity in a beginner’s profile over time.

For students, these products combine access, guidance, and gradual progression, making them a practical choice when used thoughtfully and strategically.

Entry-Level Unsecured Cards for New Credit Profiles

Unsecured cards for beginners do not require a deposit, but approval standards are slightly higher. These cards are often targeted at individuals with stable income but minimal credit history. In many cases, applicants may include recent graduates or young professionals who are new to borrowing but financially organized.

The main benefit of unsecured entry-level cards is flexibility. Without a deposit, cardholders can preserve cash while still accessing credit. This can be especially useful during the early stages of financial independence, when liquidity matters. However, limits are usually modest, reflecting the issuer’s cautious approach and the need to control early risk exposure.

Interest rates on these cards tend to be higher than average. This makes disciplined repayment essential. For novice who pay balances in full each month, the interest rate becomes less relevant, but it remains a risk factor if habits slip or expenses unexpectedly rise.

Many entry-level unsecured cards offer basic rewards, such as flat-rate cash back. While appealing, novice should treat rewards as secondary. The primary objective remains building consistent positive history and demonstrating reliable payment behavior over time.

Approval for these cards often depends on income verification and banking relationships. Some issuers favor applicants with existing checking or savings accounts, viewing that relationship as a signal of reliability and ongoing financial stability.

For learner ready to manage credit responsibly without a deposit, these cards offer a balanced entry point, provided spending remains controlled and financial discipline is maintained from the start.

Comparing Features That Matter Most for Beginners

When evaluating credit cards for beginners, certain features consistently outweigh others. Understanding these priorities helps filter out marketing noise and focus on long-term value rather than short-term appeal.

Key considerations include: Annual fees that may reduce the card’s usefulness during early stages, especially when benefits are limited, reporting to all major credit bureaus to ensure consistent credit building and accurate tracking and clear upgrade paths to better products as credit improves and experience grows

Another important feature is customer support and account management tools. Novice benefit from intuitive apps, automatic payment options, spending alerts, and responsive service that reduce the risk of missed payments or confusion.

Transparency is essential. Cards with clear terms, simple reward structures, and predictable billing cycles support learning and confidence. Complex rules, rotating categories, or hidden conditions increase the likelihood of mistakes and frustration.

Promotional offers should be approached cautiously. Introductory bonuses or temporary incentives may look attractive but should never encourage unnecessary spending or debt accumulation during the learning phase.

By focusing on practical features rather than perks, novice can choose a card that supports growth, stability, and financial education rather than distraction.

Using Your First Credit Card Responsibly

Approval is only the first step. How a beginner uses a card determines whether it becomes a financial asset or a liability. Responsible use centers on consistency and restraint, especially during the first months of account activity, when patterns are closely observed.

Keeping balances low relative to the credit limit is fundamental. Small, regular purchases that are paid in full each month demonstrate reliability without increasing risk. Routine expenses, such as subscriptions or utilities, are often ideal because they are predictable and easy to manage.

Payment timing matters. Paying before the due date, or even before the statement closes, helps maintain favorable account metrics and avoids interest charges. Early payments can also reduce reported balances, reinforcing a disciplined profile.

Tracking spending builds awareness. Beginners should treat credit purchases as deferred payments, not additional income. This mindset prevents overextension and encourages deliberate decision-making with each transaction.

Avoiding unnecessary applications is also important. Each new account adds complexity and may temporarily affect approval odds for future credit products. Allowing time between applications supports stability.

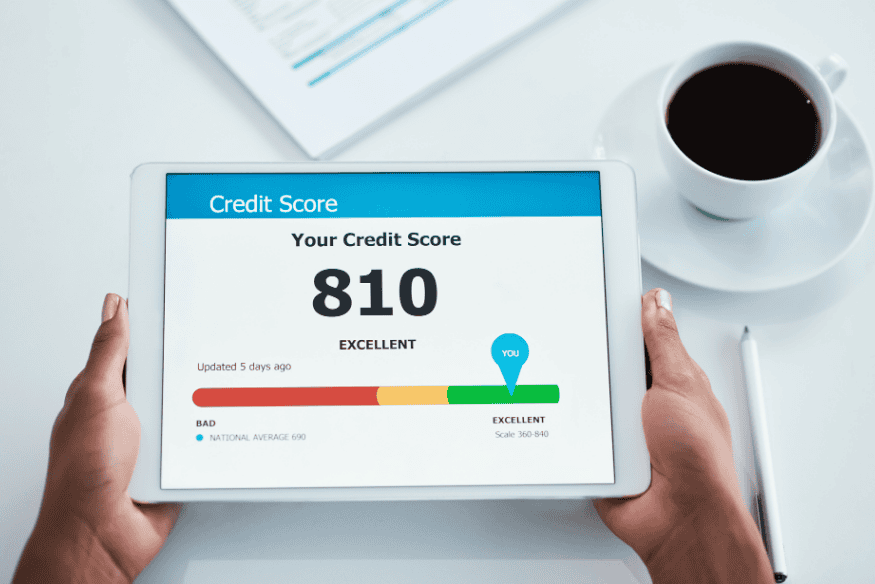

Over time, consistent habits establish a strong reputation with lenders. This reputation unlocks better terms, higher limits, and broader options as confidence in the borrower steadily increases.

How Credit Cards for Beginners Fit Into Long-Term Credit Building

A first card is not an isolated product but part of a longer financial trajectory. Early decisions influence outcomes for years, affecting access to future credit, borrowing costs, and financial flexibility during important life stages such as moving, studying, or investing.

Maintaining accounts over time contributes to a stable profile. Even when upgrading to better cards, keeping the original account open can preserve valuable credit history. The age of an account signals continuity and patience, both of which are viewed favorably by lenders and scoring systems.

As experience grows, novice may diversify with other products such as installment loans or additional cards. The foundation built with early responsible use supports these transitions, reducing rejection risk and improving terms as financial complexity increases.

Lenders increasingly rely on automated systems informed by credit bureau data from organizations like Experian and scoring models developed by FICO. Early behavior strongly influences how these systems assess risk, often setting a baseline that follows consumers for years.

Ultimately, credit cards for beginners are tools for learning and adaptation. Used wisely, they transform initial access into opportunity, reinforce healthy financial habits, and support long-term financial stability and independence.

Conclusion

Choosing the right first credit card is a strategic decision that shapes your financial future. For beginners, the best card is not defined by rewards or prestige but by its ability to support learning, discipline, and steady progress over time, especially during the earliest stages of credit building.

Secured cards offer structure and accessibility, student cards combine education with opportunity, and entry-level unsecured cards provide flexibility for those ready to take the next step. Each option serves a purpose depending on personal circumstances, income stability, and readiness to manage credit independently and responsibly.

Responsible use matters more than the card itself. Consistent payments, modest balances, and a long-term mindset transform a simple account into a foundation for broader financial goals. Over time, these habits open doors to better products, higher limits, and lower borrowing costs across different credit needs.

If you are starting your credit journey, approach your first card as a training tool. Choose thoughtfully, use it intentionally, and focus on habits rather than perks. With patience, awareness, and discipline, your earliest credit decisions can support lasting financial confidence, stability, and greater financial flexibility in the future.