Common Financial Mistakes Americans Make and How to Avoid Them

A practical 2026 personal finance guide to the most common money mistakes Americans make and how to avoid them.

Most financial problems in the U.S. don’t start with one huge decision. They start with small habits that feel harmless in the moment: carrying a balance “just this month,” skipping a savings transfer because something came up, accepting a bank fee because it’s only a few dollars, or putting off investing until life feels less busy. Over time, these choices compound—often faster than income grows—and people end up working harder just to stay in place.

The good news is that personal finance is less about perfection and more about preventing predictable mistakes. In 2026, the basics still matter: spending with intention, building resilience for emergencies, using credit strategically, protecting what you have, and investing consistently. What’s changed is the environment. Subscriptions, buy-now-pay-later offers, high-cost financing, faster payment systems, and constant marketing pressure make it easier to lose track of where your money is going. At the same time, tools like real-time alerts, automatic transfers, and low-cost investing platforms make it easier than ever to build a simple system that runs in the background.

This article breaks down the most common money mistakes Americans make—and, more importantly, the practical fixes that work in real life. You’ll learn how to create a budget you can actually follow, stop high-interest debt from quietly draining your paycheck, protect your credit score without obsessing over it, and build a plan that keeps you moving forward even when life gets expensive. If you want fewer financial surprises and more control over your future, these personal finance fundamentals are a strong place to start.

Mistake 1: Treating a Budget Like a Restriction Instead of a Tool

Many people avoid budgeting because they assume it means saying “no” all the time. In reality, a good budget is permission to spend—because you’ve already decided what matters most. The real mistake isn’t failing to track every dollar. It’s spending without a plan and hoping the math works out.

A budget usually fails for one of two reasons. Either it’s too complicated, or it’s too strict. If your plan requires daily tracking, it’s easy to quit after a busy week. If it leaves no room for fun, it creates rebound spending. A practical approach is to focus on categories that actually move the needle: housing, transportation, food, debt payments, and savings. Everything else can be simplified.

The easiest system for most households is a “fixed plus flexible” structure. Fixed costs are bills you must pay. Flexible costs are variable categories you can adjust. Once fixed costs are covered, you assign a realistic limit to the flexible categories and automate savings before you start spending.

To make budgeting stick, keep it simple and visible. Use a weekly check-in that takes ten minutes: compare what you planned with what actually happened, then adjust next week’s plan. The point is not to punish yourself for deviations. The point is to catch problems early—before you’re relying on credit to get to payday. In personal finance, consistency beats intensity almost every time.

Mistake 2: Living Without an Emergency Fund That Matches Real Life

An emergency fund is not just for job loss. It’s for the normal surprises that disrupt your cash flow: car repairs, medical costs, travel for family needs, home maintenance, and temporary income dips. The mistake is assuming emergencies are rare—and then using debt as the default backup plan.

A common barrier is thinking you need a large number before it “counts.” In practice, a small starter fund can prevent the most expensive outcomes, like overdraft fees or high-interest balances. Building that first cushion quickly creates momentum because you feel less fragile, which reduces financial stress and impulsive decisions.

Once you have a starter cushion, scale it based on your risk level. Stable income and strong insurance may allow a smaller target. Variable income, single-income households, or higher responsibility (kids, dependents) typically require more protection. The right number is the amount that keeps you from reaching for credit when life happens.

Where you keep the fund matters too. It should be separate from daily spending but still accessible. A high-yield savings account is often a strong choice because it’s liquid and keeps the money from blending into your checking balance. The best strategy is automation: transfer a set amount right after payday, then increase it gradually when you get raises or pay off debts. This is one of the highest-return habits in personal finance because it prevents expensive chain reactions.

Mistake 3: Carrying High-Interest Debt Because It Feels Normal

High-interest debt often grows quietly. Minimum payments make it feel manageable, and interest accrues in the background. The mistake is treating revolving balances as a long-term financing tool rather than an expensive short-term bridge.

If you carry balances, you need two plans at the same time: a payoff plan and a behavior plan. The payoff plan is your strategy for reducing the balance. The behavior plan prevents the balance from reappearing once you start making progress.

Two payoff methods work well for most people. The avalanche method targets the highest interest rate first, saving the most money over time. The snowball method targets the smallest balance first, which can create motivation quickly. Either works if you commit. What matters most is consistency and avoiding new balances during the payoff process.

It also helps to identify the patterns behind the debt. Some balances come from emergencies, which points back to savings. Others come from recurring overspending, which points back to budgeting. In 2026, subscription creep and “small monthly payments” are major drivers of overspending because they feel invisible. Reviewing recurring charges every quarter can free up money without changing your lifestyle dramatically.

If you’re overwhelmed, focus on one high-impact move: stop the bleeding. Freeze unnecessary spending categories temporarily, set up automatic minimum payments to avoid late fees, then direct every extra dollar to your chosen payoff target. Momentum builds faster than you think when the plan is clear.

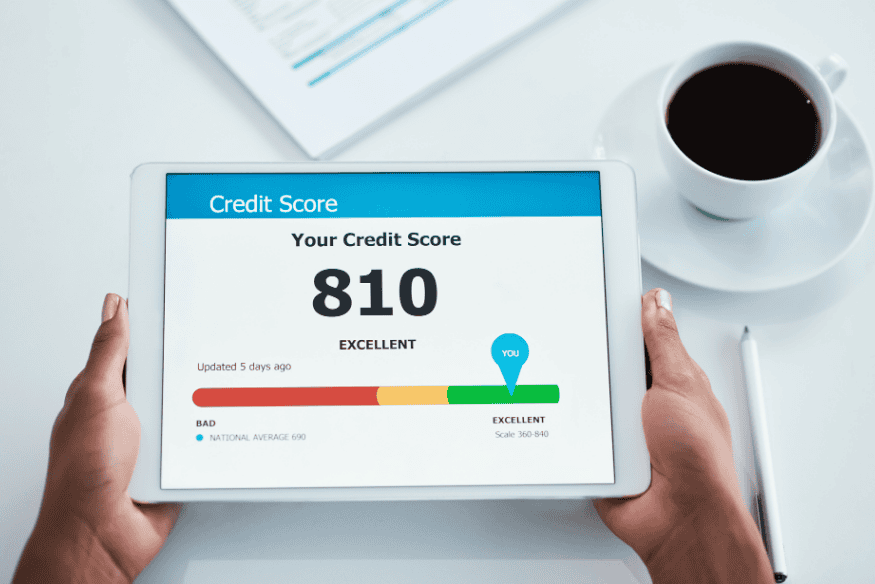

Mistake 4: Damaging Credit Through Avoidable Errors and Neglect

Credit problems aren’t always caused by irresponsible spending. They’re often caused by small mistakes: missed payments, high utilization, too many applications in a short period, or ignoring errors on a credit report. The mistake is treating credit as something you only deal with when you need a loan.

Payment history is powerful because even one late payment can have lasting effects. The simplest solution is to automate payments for at least the minimum due. Then set alerts a few days before the due date so you can adjust if needed. This reduces risk without requiring daily attention.

Utilization is another common trap. Using a high percentage of your available credit can lower your score even if you pay on time. Many people assume paying in full once per month is enough, but timing matters. If you spend heavily during the month and the statement closes with a high balance, your reported utilization may look worse than your actual behavior. A mid-cycle payment can keep utilization lower.

It’s also easy to hurt your score by applying for multiple accounts quickly. “Shopping around” for certain loans can be treated differently than revolving credit applications, but it’s still wise to be deliberate. Apply when you have a clear purpose, and avoid stacking applications during a short window unless you understand the scoring impact.

Finally, credit reports can contain errors. Checking your reports periodically helps you catch issues before they affect approvals or rates. You don’t need to obsess. You just need a routine that prevents avoidable surprises, which is a core principle of personal finance.

Mistake 5: Paying Too Much in Fees Because You Never Audit Your Money

Many Americans lose money through fees that feel too small to fight: bank charges, app subscription renewals, late fees, account maintenance fees, and “convenience” add-ons. The mistake is assuming that because each fee is small, it doesn’t matter. In reality, repeated fees are one of the fastest ways to leak money.

The fix is a simple quarterly audit. You scan your transactions for anything labeled as a fee or recurring charge. Then you ask three questions: do I still use this, is there a cheaper alternative, and can I avoid it with a system change?

Bank fees are often avoidable by choosing accounts with fewer rules, using in-network ATMs, and setting up low-balance alerts. Subscription fees are often reduced by consolidating services or switching to annual plans only for tools you truly use. Late fees are reduced by automation and buffer planning. None of this requires extreme frugality—just basic maintenance.

A powerful tactic is building a “default-free” setup. Choose providers that charge fewer penalties by design: no monthly maintenance where possible, fewer overdraft triggers, and transparent pricing. Then automate the behaviors that protect you: bill auto-pay, reminders, and small weekly transfers into savings.

The goal isn’t to eliminate every fee forever. The goal is to prevent the repeatable ones that add no value.

Mistake 6: Procrastinating on Investing and Retirement Because It Feels Complicated

A common financial regret is waiting too long to invest. People often believe they need a large amount of money or expert knowledge. The mistake is thinking investing is an advanced skill, when it’s mostly about consistency and time.

The most powerful advantage you have is time in the market, not perfect timing. If you invest steadily, you benefit from compounding over years. Starting small is not pointless. It’s how you build the habit and the system.

In the U.S., many workers have access to retirement accounts through employers, and these accounts can offer significant advantages. If your employer offers a match, missing it is like turning down part of your compensation. Even without a match, consistent contributions build long-term security and reduce the stress of trying to “catch up” later.

For many people, a simple approach works best: choose diversified, low-cost options that match your risk tolerance and time horizon, then automate contributions. Complexity is not required. In fact, overcomplicating can lead to inaction. This is personal finance at its most practical: build a process you can repeat for years.

Investing is not just for retirement, either. It’s part of building long-term stability. When you invest consistently, you reduce dependence on debt and create options for future goals.

Mistake 8: Lifestyle Inflation That Turns Raises Into Stress Instead of Freedom

Lifestyle inflation is one of the most common reasons people feel broke even as they earn more. The mistake is letting spending automatically rise to match income, so financial stress stays the same at every pay level.

This isn’t about never enjoying your money. It’s about choosing upgrades intentionally. When your income increases, you can split the raise: some goes to quality-of-life improvements, and some goes to financial security. That security might mean building savings, paying off debt faster, or increasing retirement contributions.

Lifestyle inflation is also fueled by convenience spending. Food delivery, subscriptions, premium upgrades, and frequent small purchases can quietly become a second rent payment. The fix is not to cut everything. The fix is to identify the handful of categories where spending grows without adding real happiness.

A practical strategy is to “lock in” progress with automatic rules. For example, every raise triggers an increase in savings or investing contributions before you adjust lifestyle spending. That way, you benefit immediately without relying on willpower. This is a personal finance move that works because it happens before temptation has a chance.

Over time, controlling lifestyle inflation is what turns higher income into real freedom. It creates breathing room and reduces the need to borrow when life gets expensive.

Conclusion

Most financial stress comes from a few repeatable mistakes, not from a lack of intelligence or effort. The challenge is that money decisions happen in the middle of real life—busy schedules, unexpected expenses, pressure to keep up, and constant marketing that encourages spending now and worrying later. The solution is not perfection. It’s building a personal finance system that prevents predictable problems and keeps you moving forward even when things get messy.

A strong system starts with clarity. A budget is not a punishment; it’s a plan for what you want your money to do. An emergency fund reduces the chance that one surprise turns into long-term debt. A debt payoff strategy protects your income from being consumed by interest. Basic credit habits—on-time payments, reasonable utilization, and periodic report checks—make borrowing cheaper when you actually need it.

From there, you strengthen your foundation. You reduce recurring fees and subscriptions that add nothing to your life. You protect yourself with the right insurance and basic planning. You invest consistently so time can do the heavy lifting, rather than relying on future income to solve today’s decisions. And as you earn more, you avoid lifestyle inflation that keeps you stuck on the same treadmill at a higher speed.

If you want one action step to start today, make it simple and measurable: pick one mistake from this list that you recognize in your own habits, and set up one automatic fix. Automate a payment. Create a weekly check-in. Start a small transfer to savings. Increase a retirement contribution by a modest amount. Small moves compound quickly when they’re consistent. Over time, that’s how you go from reacting to money problems to running your personal finance life with confidence.