How to Choose the Best Bank in the United States for Your Financial Goals

Learn how to choose the best bank in the U.S. by aligning accounts, fees, and services with your personal financial goals.

Choosing a bank in the United States is no longer a simple decision based on proximity or brand familiarity. Over the last several decades, the American banking landscape has expanded and diversified, offering consumers a wide range of options that vary in structure, services, pricing, and digital capabilities. From large national institutions to regional banks, credit unions, and online-only platforms, the number of choices can be overwhelming.

The concept of the best bank is also highly personal. A college student opening a first checking account has very different needs from a small business owner, a family planning to buy a home, or someone focused on long-term investing. Fees, interest rates, accessibility, customer service, and technology all play different roles depending on financial priorities and life stage.

In 2026, banking decisions have become even more strategic. Digital tools allow customers to switch institutions more easily, while greater transparency has made it simpler to compare costs and services. At the same time, economic uncertainty, evolving regulations, and technological risks make it more important than ever to choose carefully. A bank relationship is not just about transactions; it shapes how efficiently you save, borrow, invest, and manage risk over time.

This article explains how to choose in the United States by focusing on alignment rather than popularity. It explores how different types of banks operate, how to evaluate fees and services, how digital and physical access affect daily banking, and how regulatory protections safeguard deposits. By understanding these factors, you can identify the institution that best supports your financial goals today and adapts with you as those goals evolve.

Define Your Financial Goals Before Choosing a Bank

The first step in selecting the best bank is understanding your own financial objectives. Without that clarity, it is easy to choose an institution based on marketing or convenience rather than suitability. Financial goals influence which services matter most and which trade-offs are acceptable.

For individuals focused on everyday money management, priorities often include low fees, easy access to funds, and reliable customer support. For savers, interest rates and account flexibility become more important. Borrowers may prioritize competitive loan terms, while entrepreneurs need tools for cash flow management and business credit.

Short-term and long-term goals should both be considered. Short-term goals might include managing monthly expenses, building an emergency fund, or simplifying bill payments. Long-term goals could involve buying a home, funding education, growing investments, or planning for retirement.

Risk tolerance also matters. Some consumers prefer stability and in-person access, while others are comfortable managing finances entirely online in exchange for lower costs or higher yields. Understanding how much complexity you are willing to manage helps narrow options.

By defining what you want your bank to help you accomplish, the idea becomes clearer. It shifts from a generic ranking to a personalized fit based on function, not reputation.

Understand the Different Types of Banks in the U.S.

The U.S. banking system includes several types of institutions, each with distinct characteristics. Understanding these differences is essential when comparing options.

Large national banks operate extensive branch networks and offer a wide range of products, including checking, savings, credit cards, mortgages, and investment services. They provide convenience for customers who travel frequently or need in-person support nationwide. However, fees may be higher, and interest rates on savings are often lower.

Regional and community banks focus on specific geographic areas. They may offer more personalized service and local decision-making, particularly for small business lending. Their product range can be narrower, but relationships are often stronger.

Credit unions are member-owned institutions that typically offer lower fees and better rates. Membership may be based on location, employer, or affiliation. Credit unions often emphasize customer service but may have fewer branches or digital features compared to large banks.

Online-only banks operate without physical branches. They rely on digital platforms and often provide higher interest rates and lower fees due to reduced overhead. These banks are well suited for tech-savvy users but may be less convenient for cash transactions or in-person needs.

Each type of institution serves different preferences. Choosing the best bank involves matching these structural differences with how you prefer to manage money.

Evaluate Fees, Interest Rates, and Account Costs

Fees play a critical role in determining the long-term value of a banking relationship. Small, recurring charges can add up significantly over time and quietly erode savings.

Common fees include monthly maintenance fees, overdraft charges, ATM fees, and wire transfer fees. Some banks waive these fees under certain conditions, such as maintaining minimum balances or setting up direct deposits. Understanding these requirements is crucial.

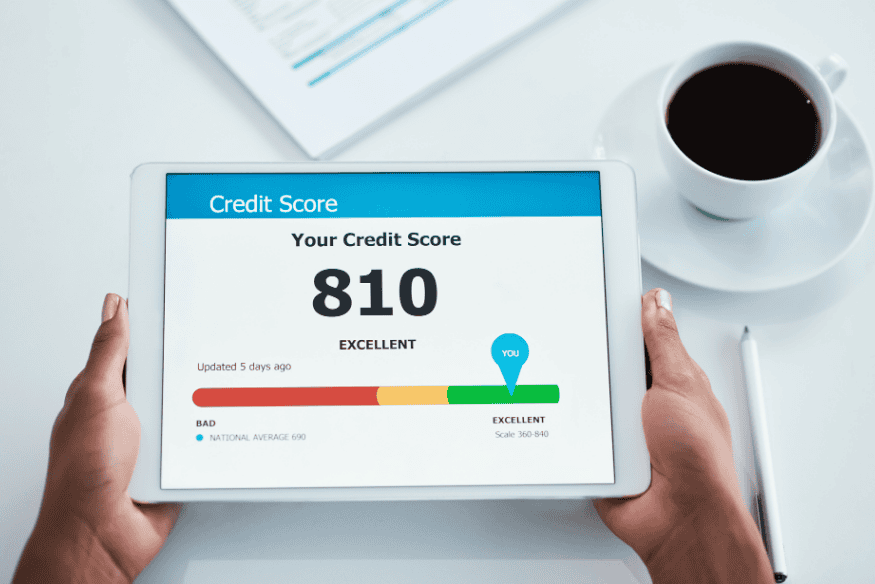

Interest rates on savings accounts, money market accounts, and certificates of deposit vary widely. While interest rate changes are influenced by broader economic conditions, some banks consistently offer more competitive yields than others. Over time, even small differences in rates can affect savings growth.

Loan rates and terms are also important if borrowing is part of your financial plan. Banks differ in how they structure personal loans, auto loans, and mortgages. Transparent pricing and flexible repayment options add value.

Comparing costs requires reading account disclosures carefully rather than relying on promotional headlines. The best bank is often the one that minimizes friction and hidden expenses while offering fair returns on balances.

Compare Digital Banking Tools and Technology

Technology has become central to modern banking. Digital capabilities influence convenience, security, and financial awareness, shaping how consumers interact with their money on a daily basis.

Mobile apps should allow customers to view balances, transfer funds, pay bills, deposit checks, and manage cards easily from one interface. Real-time alerts and spending summaries help track activity and detect potential issues quickly, reducing the chance of missed payments or unauthorized transactions.

Integration with budgeting tools and payment platforms adds efficiency. Some banks offer built-in analytics that categorize spending, highlight trends, and support goal tracking. These features can enhance financial discipline by making habits more visible and easier to adjust.

Security features are equally important. Multi-factor authentication, biometric access, device verification, and real-time fraud detection significantly reduce risk. Banks that invest consistently in cybersecurity demonstrate a strong commitment to protecting customer data and account integrity.

However, digital sophistication should match your comfort level. For some users, simpler interfaces are preferable to complex dashboards. The best bank offers technology that supports your habits, improves clarity, and adds control rather than creating confusion or unnecessary complexity.

Assess Branch Access, ATMs, and Customer Support

Despite the growth of digital banking, physical access remains relevant for many consumers. Branches and ATMs provide flexibility, especially for cash deposits, large withdrawals, document verification, or complex transactions that are difficult to resolve remotely.

If you value face-to-face support, branch availability and service quality matter significantly. Regional coverage may be sufficient for some users who rarely travel, while others benefit from nationwide access that ensures consistent service regardless of location.

ATM networks influence everyday convenience and out-of-pocket fees. Many banks offer surcharge-free access through partner networks or reimbursement programs. Understanding where and how you can access cash helps avoid unexpected costs and reduces reliance on third-party machines.

Customer support channels also deserve attention beyond basic availability. Response times, issue resolution quality, and escalation processes vary widely across institutions. Some banks excel in digital support via chat and phone, while others maintain a strong emphasis on in-person assistance.

Hybrid models are becoming more common, blending digital efficiency with limited physical presence. The importance of access ultimately depends on lifestyle, mobility, and financial habits. Evaluating these factors ensures that the best bank supports you consistently, not just occasionally or in ideal situations.

Consider Safety, Regulation, and Deposit Protection

Safety is a non-negotiable aspect of banking. In the U.S., legitimate banks operate under strict regulatory frameworks designed to protect consumers, ensure financial stability, and maintain confidence in the overall system. These safeguards apply regardless of whether the institution operates primarily online or through physical branches.

Deposits are typically insured through the Federal Deposit Insurance Corporation or the National Credit Union Administration for credit unions. This insurance protects customer funds up to specified limits in case of bank or credit union failure, creating a critical safety net that separates personal finances from institutional risk.

Regulatory oversight further reinforces protection. Agencies such as the Office of the Comptroller of the Currency supervise national banks, setting operational standards, monitoring capital adequacy, and enforcing compliance with consumer protection laws. State banking authorities and federal regulators work together to identify risks before they become systemic.

Understanding whether your deposits are insured and how your bank is regulated provides peace of mind. It empowers consumers to make informed decisions, compare institutions confidently, and focus on financial planning rather than institutional solvency concerns.

The best bank balances innovation with compliance, combining modern tools and efficiency with rigorous oversight to ensure security without sacrificing usability or transparency.

Match Banking Products to Life Stages and Needs

Banking needs evolve over time. The best bank for a student may not be ideal for a growing family or a retiree. Evaluating how a bank supports different life stages adds long-term value and reduces friction as priorities shift.

Early-stage consumers often prioritize low-cost checking, fee-free transactions, and simple digital savings tools that support habit building. During this phase, ease of access and education tend to matter more than product depth. As income and responsibilities grow, financial needs expand.

Mid-career individuals may require a broader ecosystem, including mortgages, auto loans, investment platforms, insurance options, and more advanced credit products. Efficient integration between accounts becomes increasingly important as financial complexity rises.

Later stages may shift focus toward wealth preservation, income stability, retirement planning, and estate management. At this point, advisory services, secure access, and long-term planning tools gain relevance. Some banks offer integrated ecosystems that support customers through multiple phases, allowing gradual progression without disruption. Others specialize in specific segments and may require transitions later.

Flexibility, product diversity, and clear pathways between services enhance continuity. The best bank adapts as your financial goals change rather than forcing you to adapt to its limitations.

Weigh Reputation, Transparency, and Trust

Trust underpins every financial relationship. Reputation, transparency, and ethical practices shape customer confidence, especially in an environment where most interactions are digital and long-term commitments are involved.

Publicly available information, customer reviews, and regulatory records provide valuable insight into how banks treat customers over time. While no institution is flawless, consistent complaints, repeated regulatory actions, or unclear dispute resolutions are warning signs that should not be ignored. Patterns matter more than isolated incidents.

Transparency in pricing, communication, and policy changes demonstrates respect for customers. Banks that clearly disclose fees, explain rate adjustments, and provide advance notice of changes foster stronger, more resilient relationships. Clear language reduces misunderstandings and empowers customers to make informed decisions.

Trust also involves predictability. Reliable service, consistent policies, and fair treatment during disputes matter as much as product offerings or technology features. How a bank responds when problems arise often reveals more than its marketing materials.

Ethical practices extend beyond compliance. Responsible lending standards, data protection, and respectful customer service contribute to long-term credibility.

The best is one that earns trust through consistent actions rather than marketing claims, proving reliability not just when conditions are favorable, but when customers need support most.

Conclusion

Choosing the best bank in the United States is a strategic decision that should be guided by personal financial goals rather than generic rankings. The right choice aligns services, costs, technology, and access with how you manage money today and how you plan to do so in the future as your circumstances evolve.

By defining your objectives, understanding different types of banks, evaluating fees and digital tools, assessing access and safety, and considering long-term adaptability, you can make an informed decision. The banking relationship you choose influences daily convenience, long-term growth, and overall financial security, making it an important foundation rather than a simple transaction.

There is no universal best bank, only the best for your specific needs. Taking the time to evaluate options thoughtfully allows you to avoid unnecessary changes later and reduces friction as your financial life becomes more complex. This approach empowers you to build a banking foundation that supports your financial goals with clarity, efficiency, and lasting confidence.