How to Improve Your Credit Score Without Taking New Debt

Learn practical ways to improve credit in the U.S. without taking on new debt, using proven strategies that strengthen your score over time.

Improving your credit profile is often associated with borrowing more money. Many people assume that opening new accounts or taking out additional loans is the only way to move a stagnant credit file. In reality, that approach frequently creates more risk than benefit, especially for individuals who want stability rather than short-term gains. A strong credit profile can be built and strengthened without adding new debt, as long as the right strategies are applied consistently.

In the U.S. credit system, most scoring models focus on patterns rather than isolated actions. They evaluate how responsibly you manage existing obligations, how stable your behavior is over time, and how predictable your financial decisions appear. These factors can be improved without signing new contracts or increasing borrowing exposure. For many consumers, this approach is safer, more sustainable, and easier to maintain.

Learning how to improve credit without taking new debt is particularly relevant in an environment where interest rates remain elevated and financial uncertainty affects household budgets. Taking on new obligations under those conditions can increase stress and undermine progress. Instead, optimizing what already exists often delivers more reliable results.

This article explains how to improve credit using strategies that rely on discipline, timing, accuracy, and long-term consistency. It explores how credit scores work, what lenders actually look for, and how small changes in behavior can produce measurable improvements. Each section focuses on actionable steps that strengthen your credit profile while keeping risk under control.

Understand How Credit Scores Are Calculated

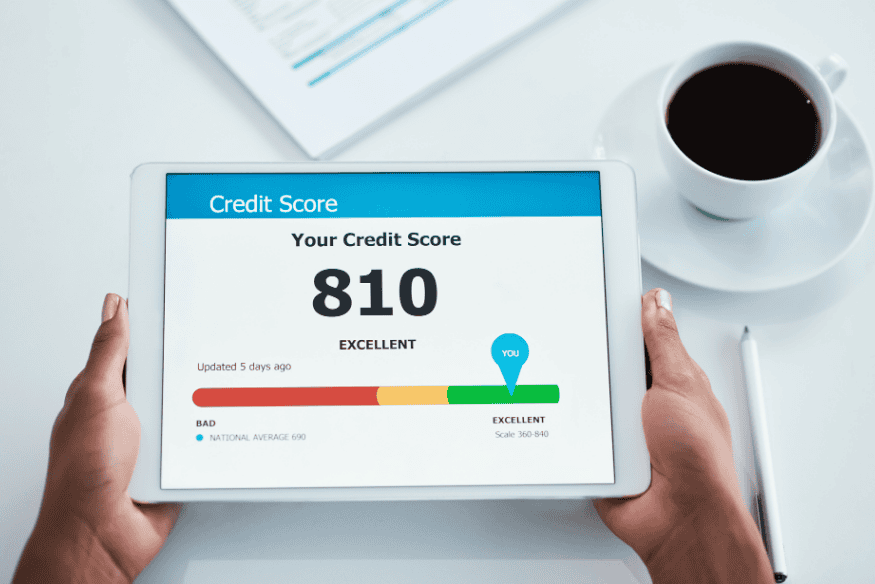

Before attempting to improve credit, it is essential to understand how credit scores are built. In the United States, credit scores are designed to predict risk. They estimate the likelihood that a borrower will repay obligations on time based on historical data and behavioral patterns.

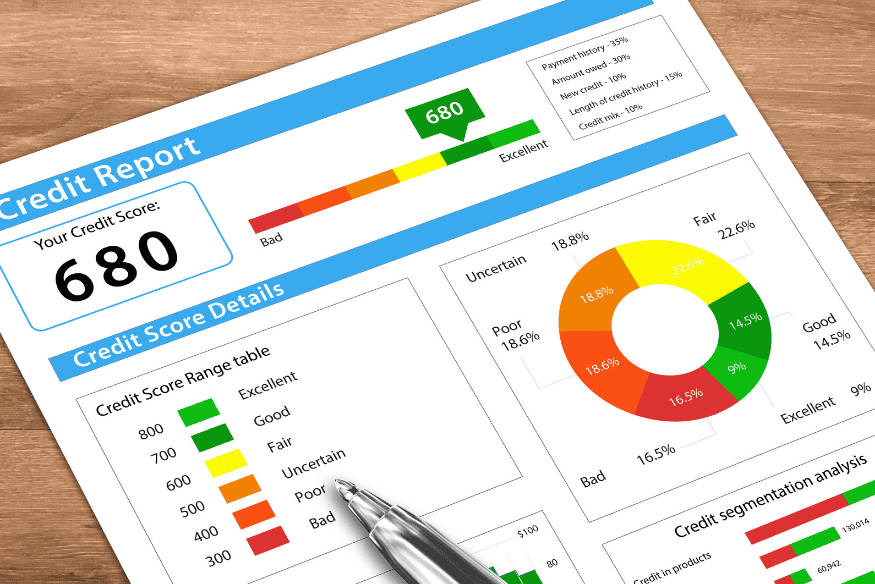

Although scoring formulas are proprietary, most widely used models evaluate similar categories. Payment history measures whether obligations are paid on time. Credit usage examines how much available credit is being used. Credit age looks at how long accounts have been open. Credit mix reflects the types of accounts on file. New credit activity tracks how frequently new accounts are opened.

Among these categories, several can be improved without adding new debt. Payment consistency, credit usage management, and account longevity are especially influential and fully controllable within an existing credit profile.

Another important point is that scores are dynamic. They change as new data is reported. This means that improvements are not limited to long time horizons. Some actions can influence your credit profile within weeks, while others require months of consistency.

Understanding that credit scoring focuses on behavior rather than intent helps clarify why new debt is unnecessary. What matters most is how reliably and responsibly you manage what you already have.

Make Every Payment On Time, Without Exception

Payment history remains the most influential factor in determining credit quality. A single missed or late payment can outweigh months of otherwise responsible behavior. Improving payment consistency is one of the most effective ways to improve credit without increasing financial exposure.

On-time payments signal reliability. They show lenders that obligations are taken seriously and managed predictably. Even small delinquencies can raise concerns, especially if they occur repeatedly or across multiple accounts.

One overlooked aspect is payment timing. Payments made a few days early are treated the same as payments made on the due date, but payments made even one day late can be reported negatively. Setting up automatic payments or calendar reminders reduces the risk of errors.

Consistency matters more than speed. Making minimum payments on time is far better for credit health than missing payments while attempting aggressive debt reduction. Over time, a clean payment record builds credibility across the entire credit profile.

If past late payments exist, their impact gradually diminishes as new positive data accumulates. Scoring models tend to weight recent behavior more heavily than older mistakes. This means that sustained on-time payments can gradually offset earlier issues without adding new accounts.

Optimize Credit Usage on Existing Accounts

Credit usage, often described as utilization, measures how much of your available credit you are using at any given time. Managing this factor is one of the fastest ways to improve credit without borrowing more money, making it a practical focus for short- and medium-term adjustments.

Lower usage signals restraint and financial stability. High usage suggests dependence on credit and raises risk indicators. Importantly, this metric is calculated using balances reported at the end of billing cycles, not intent to pay later, which is a detail many consumers overlook.

Reducing reported balances can lead to noticeable score improvements. This does not require eliminating debt entirely. Even small reductions that bring balances below key thresholds can change how the profile is interpreted by scoring systems.

Timing plays a major role. Paying down balances before statements close often results in lower reported usage, even if total spending does not change. This approach allows you to optimize reporting without altering lifestyle habits or cash flow significantly.

Another factor is distribution. Using a small portion of several accounts is often viewed more favorably than heavily using one account while others remain unused. However, spreading balances should not increase total spending or encourage unnecessary borrowing.

By focusing on how balances appear rather than taking on new obligations, it is possible to improve credit metrics efficiently, strategically, and responsibly over time.

Keep Older Accounts Open and Active

Account age contributes to credit stability. Older accounts demonstrate long-term reliability and provide more data for evaluation across different financial cycles. Closing accounts, even those no longer in use, can shorten average account age and reduce available credit at the same time.

Keeping older accounts open helps preserve this history. Even if an account is rarely used, small periodic transactions followed by prompt repayment can keep it active and prevent closure by the issuer due to inactivity.

Many people close accounts in an attempt to simplify finances, not realizing that this can negatively impact credit evaluations. The loss of an older account can affect both age and usage metrics simultaneously, creating a compounded effect on the overall profile.

There is also a behavioral signal associated with longevity. Long-standing accounts suggest stable financial relationships and consistent management. Newer accounts, even when managed well, lack that historical depth and context.

Maintaining older accounts does not require increased spending. Strategic, minimal use paired with timely payment is sufficient to preserve their positive contribution and avoid unnecessary risk.

By valuing account age as an asset, you reinforce one of the strongest foundations of a healthy credit profile and support long-term financial confidence.

Review Credit Reports for Errors and Inaccuracies

Errors on credit reports are more common than many consumers realize, especially in systems that process large volumes of financial data. Incorrect balances, outdated account statuses, duplicated accounts, or misreported late payments can all hinder efforts to improve credit and distort real financial behavior.

Regularly reviewing reports allows you to identify issues that are not reflective of actual behavior. Correcting these errors removes negative signals that scoring models interpret as risk, which can otherwise offset positive habits like timely payments and low balances.

Disputing inaccuracies does not involve taking on new debt or altering spending patterns. It is a corrective process that ensures your profile accurately represents your financial behavior. Successful disputes can result in immediate improvements once corrections are applied and records are updated.

It is important to focus on factual inaccuracies rather than legitimate negative history. Disputes are most effective when supported by documentation, payment records, and clear explanations that directly address the reported issue.

U.S. consumers are entitled to review reports from major credit bureaus such as Experian, Equifax, and TransUnion. Monitoring these reports helps maintain accuracy over time and reduces surprises.

Ensuring clean and accurate data strengthens all other improvement efforts and prevents progress from being undermined by preventable reporting errors.

Avoid New Credit Applications and Hard Inquiries

Although this article focuses on improving credit without new debt, it is also important to address inquiries. Each hard inquiry signals that new credit is being sought, which can temporarily lower scores and increase perceived risk, particularly when several occur within a short period of time.

Avoiding unnecessary applications allows your profile to stabilize. Stability is a positive indicator in credit assessments because it suggests control, planning, and the absence of urgent financial pressure. Frequent applications, even without approval, can suggest financial stress, overextension, or uncertainty about available options.

Hard inquiries typically remain visible for up to two years, with the strongest impact occurring early on. Their influence fades with time, but minimizing these inquiries helps maintain a clean behavioral record during critical evaluation periods, such as when applying for loans or refinancing.

Resisting promotional offers and unsolicited preapprovals supports long-term goals. Many offers are designed to encourage impulsive decisions that may not align with your financial strategy or current readiness to manage additional credit responsibly.

Strategic timing also matters. When new credit is necessary, grouping related applications within a short window can sometimes reduce cumulative impact, depending on the product type and scoring model.

By focusing on managing existing accounts rather than expanding credit lines, you reinforce a pattern of restraint, consistency, and measured decision-making that scoring systems tend to reward over time.

Establish Consistency and Patience Over Time

Credit improvement is cumulative. While some actions produce quick changes, most meaningful progress comes from sustained consistency. Short-term strategies are less effective without long-term discipline, because scoring systems are designed to evaluate behavior over extended periods rather than isolated adjustments.

Patterns matter more than isolated actions. A year of stable behavior carries more weight than a few months of intense effort followed by inconsistency. Credit models are built to detect trends, rewarding steady habits such as on-time payments, balanced usage, and account stability over time.

Patience reduces pressure. Attempting to force results quickly often leads to unnecessary risk, such as excessive applications or drastic financial moves. By focusing on gradual improvement, you allow positive signals to strengthen naturally and remain durable.

Consistency also builds confidence. As metrics improve, access to better financial options increases without the need for new debt. Lower rates, higher limits, and broader choices reinforce a healthy cycle of responsible management.

Small actions repeated reliably are more powerful than dramatic changes. Regular monitoring, timely payments, and controlled usage compound quietly.

Understanding that improvement is a process helps align expectations and reduces frustration. The credit system rewards reliability, persistence, and sound habits—not speed or impulsive correction.

Use Credit as a Reporting Tool, Not a Funding Tool

One of the most effective mindset shifts for those seeking to improve credit is viewing credit as a reporting mechanism rather than a source of funds. Credit usage exists to generate data, not to supplement income. This distinction helps remove emotional spending decisions from the credit-building process.

Small, controlled transactions create reporting activity without adding financial strain. Paying these balances in full turns credit into a signal of reliability rather than debt accumulation. Over time, this repeated pattern communicates stability and discipline to scoring systems.

This approach aligns behavior with how scoring models interpret data. It creates consistent positive entries without introducing risk, volatility, or dependency on borrowed money. The focus shifts from borrowing capacity to behavioral consistency.

By separating spending decisions from credit-building goals, you maintain clarity and control. Credit becomes a tool for reputation rather than consumption, reducing the temptation to overspend or justify unnecessary purchases.

Adopting this mindset also lowers stress. When credit is treated as a measurement system, progress feels more predictable and intentional. This perspective supports sustainable improvement, reinforces healthy habits, and contributes to long-term financial health and confidence.

Conclusion

Improving your credit profile does not require taking on new debt. In many cases, borrowing more complicates the situation and introduces unnecessary risk, especially when existing obligations already demand attention. The most reliable improvements come from optimizing current behavior, ensuring data accuracy, and maintaining consistency over time.

By focusing on timely payments, managing usage, preserving account age, avoiding new inquiries, and correcting inaccuracies, it is possible to improve credit steadily and responsibly. These strategies work because they align precisely with how credit scores are designed to measure risk, predict behavior, and assess reliability.

Patience and discipline are the most valuable assets in this process. Credit scoring systems reward stability over time, not short-term maneuvers or aggressive tactics. Viewing credit as a behavioral record rather than a funding source allows for sustainable progress without added pressure.

If your goal is to improve credit without increasing financial obligations, concentrate on what you control today. Small changes, applied consistently and thoughtfully, often produce results that are both meaningful, durable, and long-lasting.